Hard discount stores are coming to Venezuela: what should supermarket chains do before they arrive?

- May 4

- 9 min read

In 2009, D1 opened its first stores in Colombia with such a simple model that many executives at established chains didn't take it seriously. The assortment was limited to 700 items, almost all private label, and the stores were small with no decoration, no music, and no staff. The prices on basic items were unbeatable.

Fifteen years later, D1 surpassed Grupo Éxito in revenue. In 2024, it reported operating income exceeding 21 billion Colombian pesos, becoming the leading retailer in the country. Hard discount stores grew from representing 4% of the Colombian market in 2015 to 25% in 2026—exactly the same proportion held by established chains today.

Pedro Quintana, director of Atenas Grupo Consultor, and Amaru Liendo, president of Venamcham, agree: the hard discount format will arrive in Venezuela. It's just a matter of time. In Colombia, it took three years to become relevant and fifteen to lead the market. In Venezuela, with greater smartphone penetration, greater consumer awareness of prices, and an economic environment that rewards value above all else, the cycle could be shorter.

Venezuelan television networks today have something that Colombian networks lacked in 2009: complete information about what's coming. That window of opportunity is worth millions if used decisively. It's worthless if ignored.

What happened in Colombia with the Hard Discount movement and why established supermarket chains lost so much ground

To understand what to do in Venezuela, one must understand exactly what happened in Colombia and at what point the established chains made their most costly mistakes.

D1 didn't make a splash. It entered slowly, in working-class neighborhoods of Medellín, with 200-square-meter stores that no one considered real competition for Éxito or Jumbo. The mistake was underestimating its value proposition: for the Colombian consumer on a tight budget, D1's simplicity wasn't a limitation—it was exactly what they needed. Less time choosing between 30 different types of oil, a guaranteed lowest price, and a store close to home.

Nielsen's data tells the story accurately. Between 2013 and 2018—just five years—chain hypermarkets lost 8% of their market share. The traditional neighborhood store channel lost 7 percentage points. D1, Ara, and Justo y Bueno captured all of that space.

By 2026, the landscape had solidified in a way few in 2009 could have imagined: hard discount stores accounted for 25% of Colombian retail. Established chains also represented 25%. The remaining 50% was distributed among minimarkets, specialty stores, and other formats.

Éxito—which in 2015 sold nine times more than D1—was overtaken by the discounter in 2024. The correct interpretation of this data is not that Éxito failed. It's that D1 grew at a rate that no traditional business model can replicate when it has access to capital and operates with a radically lower cost structure.

The relevant question for Venezuela is not if hard discounting will arrive. It's when. And what Venezuelan chains should do with the time they have before that happens.

The four mistakes Colombian supermarket chains made — and that Venezuelan chains can avoid

The investigation into the response of Colombian chains to hard discount reveals four errors that are repeated with a consistency that turns the case into a manual of what not to do.

1: Trying to compete on price

The initial response of many Colombian chains was to lower prices in the categories where D1 was taking market share. This was the wrong strategy for a simple reason: hard discounters have a cost structure that a chain with a wide assortment, multiple formats, and loyalty programs can never replicate. D1 carries 700 SKUs. Éxito carries 30,000. The cost per square meter, per SKU, and per employee is radically different. An established chain that lowers prices to compete with the discounter only erodes its own margin without closing the price gap.

2: Underestimating the speed of expansion

D1 started slowly. But once it had the capital—with the investment from the Santo Domingo Group in 2015—it accelerated so rapidly that no established chain could keep up. By 2019, it had 1,300 stores and plans to open 400 more in a single year. The discounter sets up shop in neighborhoods where established chains don't operate because the larger format isn't profitable in those areas. When the larger chains tried to respond with smaller, neighborhood-oriented formats, they found the discounter already established and with a loyal customer base.

3: Delaying the decision on private label brands

66.6% of D1's sales are private label brands. This is what allows them to offer unbeatable prices while maintaining profit margins. Established Colombian chains took years to respond with a serious private label strategy—not only in terms of price, but also quality and targeting premium segments. When Carulla Fresh Market and Éxito Wow got it right, sales doubled in the rebranded stores. But the delay cost them market share that they never recovered.

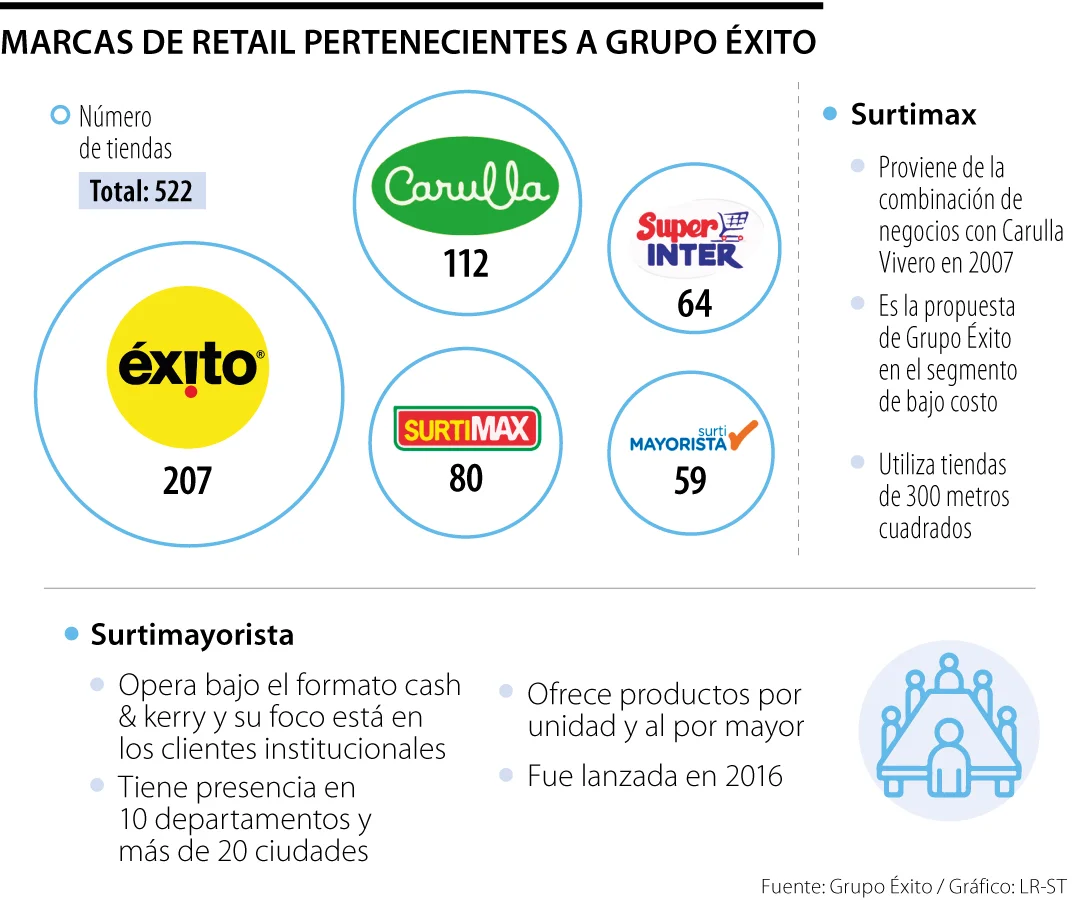

4: Fragmenting the brand portfolio instead of simplifying it

Grupo Éxito once operated five brands simultaneously—Éxito, Carulla, Surtimax, Surtimayoristas, and Super In—with confusing value propositions and scattered marketing resources. Compared to the absolute clarity of D1's message, this complexity was a disadvantage. The decision to simplify to two brands—Éxito for hypermarkets and Carulla for supermarkets—came too late, but when it did, it yielded results. Carlos Calleja, president of Grupo Éxito, confirmed in January 2026 an investment of $150 million for that year—almost double the amount allocated for 2025—driven by this new strategic clarity.

The four decisions that Venezuelan supermarket chains must make now to face the Hard Discount

With that clear diagnosis, Venezuelan chains now have the possibility of doing what Grupo Éxito, Jumbo and Olímpica could not do in 2009: prepare before the format arrives.

These are the four specific decisions that will determine who will win that game when the time comes.

1: Redesign the assortment with a value-based logic, not a variety-based one.

Hard discount stores succeed with 700 product lines because they meet 80% of consumers' basic needs at unbeatable prices. Established chains cannot and should not try to do the same. But they can—and should—conduct a rigorous review of how many of their products actually generate turnover and profit, and how many are on the shelf simply due to commercial inertia.

In category management projects that TMC has carried out with chains in Latin America, we consistently found that between 25% and 35% of the active SKUs in a chain generate less than 5% of category sales. This underutilized shelf space is the space that the discounter will occupy when it arrives—not physically, but in the mind of the consumer who perceives that the large chain has a lot but doesn't have what they're looking for at the right price.

Assortment rationalization—identifying essential, differentiating, and dispensable items in each category—is the first decision a chain must make before hard discounting arrives. After it does, under the pressure of declining sales, it becomes much more difficult and costly.

2: Build a serious private label brand strategy — especially in premium segments

The most important lesson from the Colombian case is not that private label brands at a competitive price work—that was already known. The lesson is that private label brands in premium segments are the most effective weapon an established chain has to differentiate itself from discounters and protect its profit margin at the same time.

Carulla Fresh Market and Éxito Wow focused on experience, high-quality fresh products, and premium private labels. These stores doubled their sales. Consumers looking for the best price go to the discount store. Consumers looking for quality, freshness, and trust go to the chain that offers that. The mistake to avoid is trying to be both at the same time without a clear understanding of which market segment you're actually competing in.

For Venezuelan supermarket chains, this has a concrete implication: 90% of the products on Venezuelan shelves are domestically produced. This presents a huge opportunity to develop private label brands with local suppliers in high-consumption categories—dairy, processed meats, snacks, cleaning products—before the discounter arrives and gets there first.

3: Be the first to reach the neighborhoods where the discount store will be located

Hard discount stores don't compete for the same shelf space as large chains. They compete for the neighborhood, the corner store, the five-minute walk from home. D1 set up shop in neighborhoods where Éxito wasn't present because the larger format wasn't profitable in those areas. When Éxito tried to respond with Carulla Express and smaller, more convenient formats, the discounter was already established.

Venezuelan chains know their markets and their cities. They know which neighborhoods in Caracas, Valencia, or Maracaibo have high consumer density and low penetration of modern retail channels. These are precisely the neighborhoods where the discounter will open first. And the chain that arrives there first—even with a smaller, simpler format than its flagship store—will have a locational advantage that the discounter cannot easily overcome.

Opening in those spaces doesn't require the same format or investment as a full-fledged store. It requires clarity on what value proposition makes sense in that area and a willingness to operate a different format than the one the chain is familiar with.

4: Build a real loyalty program before price competition arrives

The most revealing statistic regarding the Colombian case in 2026 is this: Éxito maintains 32% top-of-mind awareness among Colombian adults, even after 15 years of aggressive competition from hard discounters. This resilience doesn't stem from price—it comes from Puntos Colombia, the loyalty program that creates a real switching cost for consumers who have been accumulating points for years.

A loyalty program built before price competition arrives has enormous strategic value: consumers who have accumulated points, receive personalized offers, and feel that the chain knows them have a concrete incentive not to switch to a discounter when it does. Those who have no connection to the chain beyond price will go to the first format that offers something cheaper.

For Venezuelan chains that do not yet have a structured loyalty program, the time to build one is now — not when the discounter arrives and the consumer already has a reason to compare.

What distinguishes the supermarket chains that are going to win

Colombian history also has a positive narrative that is just as important as diagnosing its mistakes. Grupo Éxito didn't disappear. Jumbo continues to grow. Carulla is stronger today than it was in 2015. The chains that responded well to hard discounting didn't do so by competing on price—they did it by building a value proposition that the discounter can't replicate.

The chain that will win in Venezuela when hard discount arrives isn't the biggest or the oldest. It's the one with the right assortment for every shopping need, a private label that builds trust and profit margin, a presence in the right neighborhoods, and a loyalty program that creates real bonds with its customers.

That chain exists in Venezuela today. The question is whether it will build those capabilities in time—or whether it will wait for the discounter to arrive before reacting, as the Colombian chains did in 2009.

Does your supermarket chain in Venezuela have the strategy to win that game?

The history of hard discount stores in Latin America has a recurring theme in every market where it arrived: the chains that won weren't those that reacted best when the format first appeared. They were the ones that prepared before it arrived.

In Venezuela, the conditions that caused previous attempts to fail are changing. The de facto dollarization of the economy, the recovery of consumption, the arrival of private investment, and the progressive professionalization of modern retail channels are creating an environment where hard discount stores have a greater chance of thriving than ever before.

Supermarket chains in Venezuela that make the four decisions described in this article—rationalizing their product range, developing private labels in premium segments, being the first to reach the right neighborhoods, and building a genuine loyalty program—will be in a radically different position when the new format arrives. Those that wait to react will find themselves exactly where Grupo Éxito was in 2015: chasing after a competitor that already has loyal customers.

At TMC, we have 30 years of experience working with retail chains in Latin America on category management, private label development, ideal store design, and joint business partnerships with manufacturers. We have documented cases of sales per square meter improvements of up to 25%.

If you want to assess how your supply chain is positioned for the upcoming scenario, the first step is a 30-minute conversation.

Sources consulted

AmericaMalls & Retail. "Hard Discount War in Colombia." AmericaMalls, February 2026. americaretail-malls.com

Colombia Retail / La República. "D1, a decade of expansion and leadership in Colombian retail." Colombia Retail, September 2025.colombiaretail.com

Portafolio. "Grupo Éxito gives its Carulla supermarkets a makeover: reveals 2026 investment." Portafolio, January 2026. portafolio.co

Pulzo. "Éxito maintains its leadership with 32% among adults, D1 among young people." Pulzo, May 2026. pulzo.com

Pulzo / NielsenIQ. "D1, Ara, Éxito Supermarkets and Private Label Products in Colombia 2025." Pulzo, June 2025. pulzo.com

PREDIK Data-Driven. "Panorama of Hard Discount in Latam." PREDIK, September 2025. predikdata.com

TalCual Digital / Atenas Consulting Group. "Low-cost supermarkets: a regional trend trying to gain traction in Venezuela." TalCual, January 2025.talcualdigital.com

Ad-Gnosis. "The influence of discounters on changing consumption habits of Colombians." Dialnet, 2019. dialnet.unirioja.es

Colombia Retail. "4 strategies of Colombian supermarkets against hard discounters." Colombia Retail, September 2024.colombiaretail.com

Comments